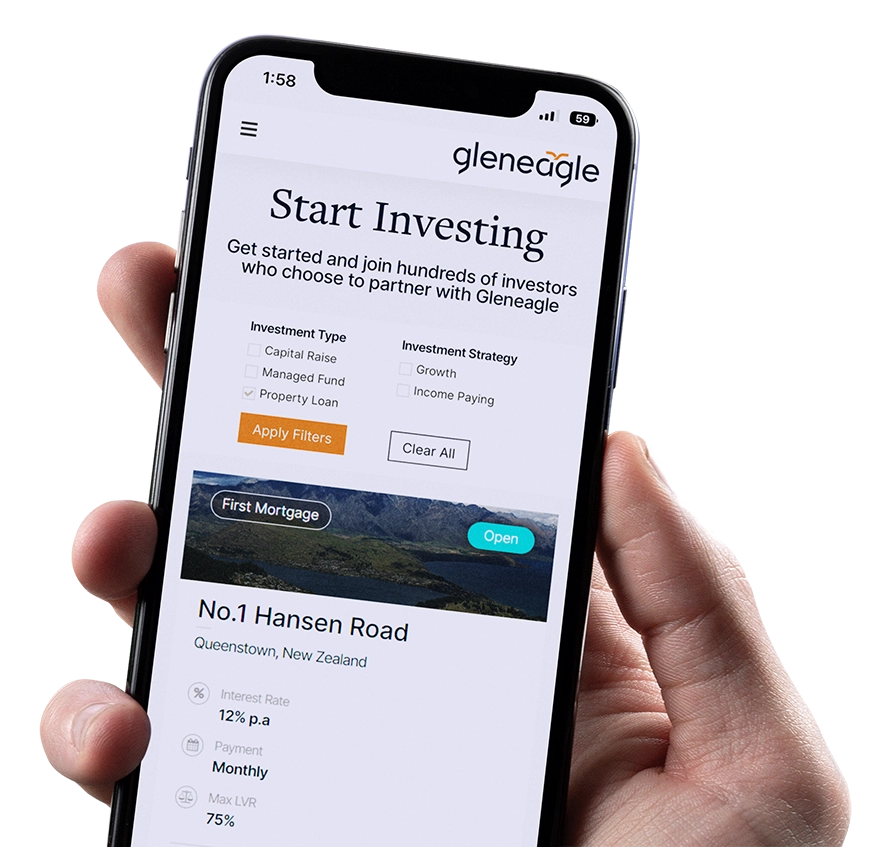

Every deal is subject to our extensive credit assessment, compliance, and underwriting conditions. Each year, only a select few meet our strict criteria.

We only present you with the deals we’re confident having in Gleneagle’s own portfolio.

Managed Funds pool together funds with other investors and provide access to immediate diversification and economies of scale.

Choose a fund that meets your individual investment objectives and risk profile, including choices of high growth equity strategies and income paying products.